Baker Tilly COMPASS

Comprehensive federal, state and local funding solutions for public sector entities at any point of your strategic funding journey.

The American Rescue Plan Act of 2021 (ARP) Final Rule establishes a staggered reporting schedule based on entity type. If your state or local government entity falls into one of the following categories, your first Project and Expenditure (P&E) report is due by Jan. 31, 2022.

NOTE: lesser populated cities and counties have until April 30, 2022 to submit their first P&E report.

This report will address obligations and expenditures that occurred from March 3, 2021 to Dec. 31, 2021. Subsequent P&E reports will cover one calendar quarter and be submitted within 30 calendar days of the end of each calendar quarter. The final P&E report will be due on March 31, 2027.

Governmental entities not described above are required to submit the first P&E report by April 30, 2022, with additional reports due annually through April 30, 2027. For many reporting in April, this will be the first occasion to use the U.S. Treasury’s (Treasury) reporting portal. It is wise to begin the process now, as it typically takes significant time to complete the registration process. Instructions for registration were sent to non-entitlement units in mid-December 2021. Information regarding registration can be found at the Treasury’s Coronavirus State and Local Fiscal Recovery Funds website.

Like the interim report submitted in August 2021, the P&E report will be conveyed to the Treasury through its electronic portal. On Jan. 7, 2022, the Treasury released the Project and Expenditure Report User Guide. The guide expands on Treasury’s Nov. 15, 2021 Compliance and Reporting Guidance.

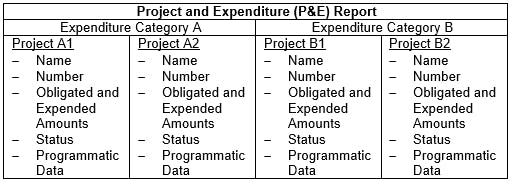

The P&E report is organized around 66 Expenditure Categories (ECs) listed in Appendix C of the Project and Expenditure Report User Guide. “Projects” uniquely created by each SLFRF recipient will be assigned to an EC. These projects are defined as “a grouping of closely related activities that together are intended to achieve a specific goal or directed toward a common purpose.” Descriptive, financial and programmatic data is provided for each project. The following figure describes the P&E report structure.

States, territories and entities with populations over 250,000 will be required to enter a budget for each project. Future P&E reports will require demographic distributions of the population served.

Contracts, grants, loans, transfers or direct payments greater than $50,000 will require separate entry into the P&E report portal and will be linked to projects through identification of the associated project names and numbers. Transactions less than $50,000 are reported in aggregate.

NOTE: for subrecipients not registered on www.SAM.gov, it may be necessary to report compensation for the five highest paid subrecipient officers.

Many of the ECs require reporting of certain programmatic data. For example, for projects associated with “Rehiring Public Sector Staff” (EC 2.14), entry into the P&E report will require identification of the number of full-time equivalents rehired. Infrastructure projects that cost over $10 million require provision of information related to Davis Bacon prevailing wage and Project Labor Agreement Certification. Adherence to Davis Bacon prevailing wage requirements and execution of a project labor agreement are not required. However, in their absence, recipients are asked to provide alternative information.

The P&E report has the one-time option for entities to elect up to a $10 million standard allowance for revenue loss or continue to calculate revenue loss using the prescribed formula. Reporting requirements are reduced for expenditure of revenue loss dollars. A narrative description of how revenue replacement dollars were allocated is all that is required.

Count on Baker Tilly’s specialized public sector Value Architects™ to help your entity navigate SLFRF reporting requirements to ensure compliance with federal funding administration. Our team continues to stay up-to-date on the latest ARP developments and is available to assist you in preparing compliance reports. (Note: some entities report quarterly and others report annually.)

For more information, or to learn more about how Baker Tilly can help your entity, contact our team.

U.S. Treasury, Project and Expenditure Report User Guide, Jan. 7, 2022

Comprehensive federal, state and local funding solutions for public sector entities at any point of your strategic funding journey.