Mapping the relationship between production data to revenue and costs with Dynamic Costing®

Much of the talk in manufacturing these days is focused on Industry 4.0, artificial intelligence (AI), Internet of Things (IoT) and 5G — tools and concepts that will revolutionize manufacturing.

While there’s no denying the potential of these innovations, we’d like to talk about something that tends to get buried underneath all of the hype: business 101. More specifically, the ABCs of business 101: the relationship of profits to revenue and costs.

To manufacturers, A-B=C; Revenue - Cost = Profit. And, yet, despite the simplicity and elementary nature of this reality, if you were to ask many manufacturers to identify their most profitable items, they would not be able to do so. They might be able to provide general insight of profitability based on their understanding of their standard costs, which are estimates of the actual costs in a company's production process. But they could not tell you which items are most profitable — in part because they do not understand the dynamics of cost.

As seen most recently during the COVID-19 crisis, when supplies, materials and even the workforce itself was disrupted and manufacturers had to make hard decisions about which items to manufacture and in what quantities, the need to know dynamic costs became critical.

Dynamic Costing® marries real-time production data from the shop floor to financial revenue and cost data to give you greater insight into profitability.

Dynamic Costing versus standard costing

The main components of traditional standard costing — labor, materials, fixed overhead and variable overhead — only tell part of the story when it comes to determining the true cost of a product. It omits several contributing elements that should factor into your business’s actual costs. The standard costing approach may even damage a manufacturer’s bottom line by not having a proper understanding of which products are responsible for driving profitability.

Dynamic Costing represents an opportunity for manufacturers to improve revenue, cost and profits because of the underlying tools and technologies found today on the shop floor, namely, manufacturing execution systems (MES). MES effectively take data directly from production machinery, providing us with information on output in a near real-time manner and allowing manufacturers to see the physical activity on the shop floor. By combining production data with financial revenue and cost data, companies are able to see more dynamically their actual costs.

Dynamic Costing is not so much a technology (although it relies heavily on technological components) as it is a discipline. By understanding your costs for manufacturing in a dynamic sense (daily, rather than annually) and integrating it into your business processes, you can better understand where revenue and profits are generated throughout your product families.

Variances

It’s hard to understand how well you are manufacturing something if you can’t determine your variances. At one level, you should know your performance between actual and standard costs. Those variances should all have explanations as well.

Too often, however, the lack of timely data means that companies won’t necessarily spot many variances until after the month or the variances in one batch are averaged or blended into those of other batches. By the time you get the information, it’s too late.

Worse yet, there will be many disagreements as to whether a variance actually means anything. For example, if the production mix this month included a number of more complex products but the cost accounting standard used is based on an average of all kinds of products, you’ll get inaccurate variance data.

Shorter time increments and better data sources mean that companies can get real-time actual costs and compare them to more precise standard costs. The goal of this is to spot anomalous production issues (e.g., too much machine setup time, excess scrap being generated or unexpected machine down time) in as close to real-time as possible.

The reality for a manufacturer is that every day you are making more or less of something than anticipated. As a result, your cost standards are a good proxy for what you are doing. But unless you're refreshing them daily, you are really not getting at the root of how they’ve changed.

Fast forward to COVID-19 where, because of constraints resulting from limits on materials, supplies and manpower, standard costs suddenly do not reflect actual costs. This may be driven by making much less than what you anticipated and with higher unit costs. Cost standards likely don't reflect this reality.

That's one trigger.

Another issue is limited plant capacity. Every manufacturer is trying to get more out of its plants. If you are limited by capacity, what should you make more of? What should you eliminate?

Dynamic Costing: our approach

Dynamic Costing is not a technology — although it contains a technological dimension. Instead, it's a combination of cost accounting metrics, analytics as well as an understanding of manufacturing and distribution. Ultimately, before you can even begin to build a technical solution addressing these dynamics, you need to understand all three: your bills of material, your physical production routings and how costs are applied through your accounting ledger.

As you start to extract your production machinery data into a centralized location, such as a cloud or on-premise database, you will eliminate inefficient and outdated Excel-based reporting. That aggregated centralized repository then becomes the gold standard source of truth, rather than a disaggregated entanglement of spreadsheets. This facilitates precise, highly available analytics for production, revenue and costs, which is the ultimate goal of Dynamic Costing.

To move toward Dynamic Costing, companies need some tools, which include Industry 4.0 enablers. Data analytics is one enabler that will provide manufacturers with statistically meaningful information. With proper integration, manufacturers can have improved transparency among departments; data accuracy, with reduced errors and time dedicated to manual processes; real-time data providing stakeholders access to critical data in one place whenever they need it; and automation, which eliminates redundancies and increases efficiencies.

Another important step is establishing an extract, transform and load (ETL) process workflow. With an ETL workflow tool, one can integrate manufacturing data: materials used, labor time, etc. This allows for disparate yet vital data to land in a clean, dynamic analytic with significant horsepower.

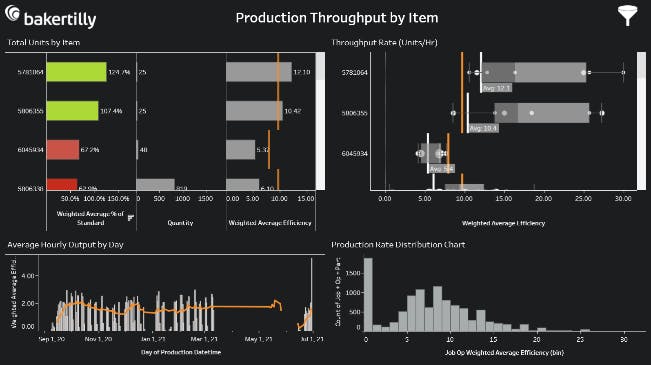

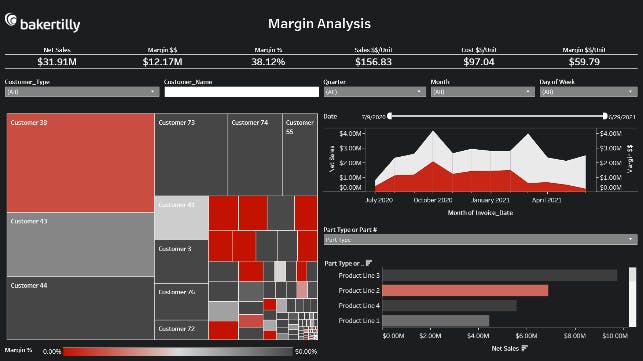

Visualizing Dynamic Costing

Dynamic Costing enables visual analytics, including but not limited to those shown above. In the end, companies need to be able to see and understand their profitability at the customer and manufactured-item level more frequently than they have in the past. Baker Tilly is here to help you create visibility to your costing data and, more importantly, map how that costing data flows into the company’s financial statements.