Article

Tax benefits of REITs for real estate firms, sponsors, and investors

July 26, 2023 · Authored by Lillian Chen

As real estate investment trusts (REITs) proliferate in both public and private real estate sectors, there’s a growing list of benefits they can provide when compared to partnerships, including REIT real estate investments.

REIT tax overview

REITs, as corporations for income tax purposes, must own predominantly rental real estate assets or debt secured by real estate that’s held for enjoyment of income and long-term appreciation.

Dividends are tax deductible. At least 90% of net ordinary taxable income must be distributed and 100% is required to avoid REIT-level tax.

REITs can’t be closely held, as defined, and must have at least 100 shareholders. A vast and nuanced array of organizational, operational, asset, and income tests must be met.

Shareholder impact is generally straightforward. A dividend, documented on a 1099 and consisting of ordinary income and sales gains, represents their proportional share of the REIT operation for the year.

Despite the rule set complexities, REITs can be highly efficient and useful vehicles for real estate assets and debt. Note that in a fund setting, captive REITs with the common stock owned by a fund above it plus 100 direct preferred shareholders, are common structures.

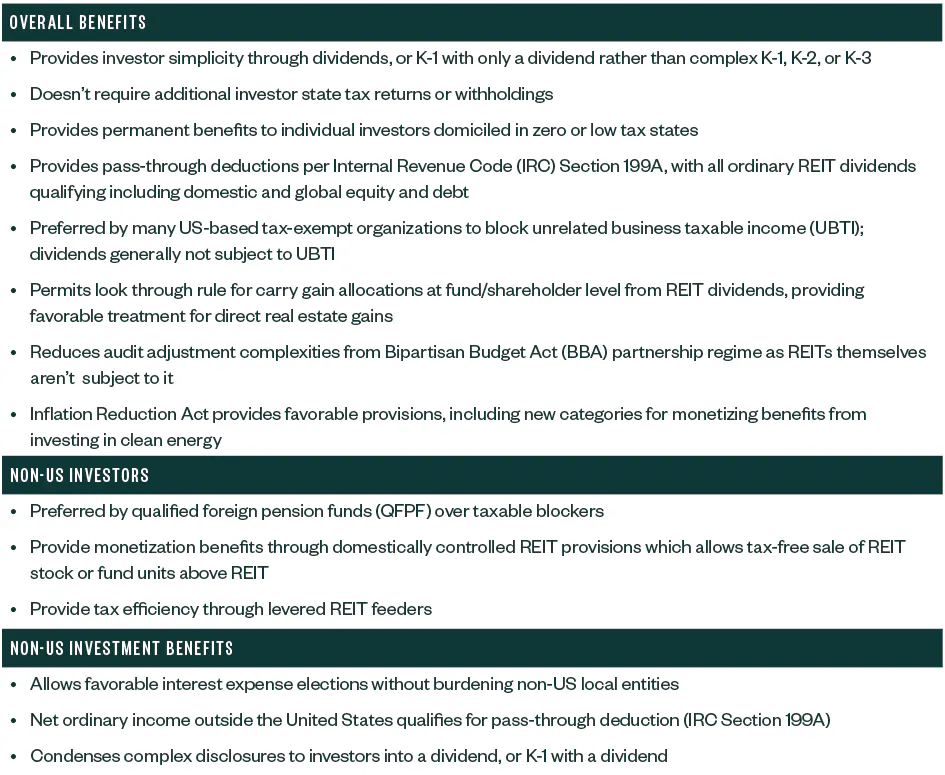

REIT benefits

REITs require high levels of administration and technical precision. Though potential downsides exist compared to partnerships, the benefits they provide can be significant, for U.S. and non-U.S. investors alike.

Overview of REIT benefits

A more in-depth look into REIT benefits follows.

State tax blocker

The REIT may have properties located in several states. It may have tax returns filed in each state, but an individual or trust shareholder would receive the dividends that are generally only taxable in the shareholder’s state of domicile with no added investor state filings or liabilities.

Related sections

The information provided here is of a general nature and is not intended to address the specific circumstances of any individual or entity. In specific circumstances, the services of a professional should be sought. Tax information, if any, contained in this communication was not intended or written to be used by any person for the purpose of avoiding penalties, nor should such information be construed as an opinion upon which any person may rely. The intended recipients of this communication and any attachments are not subject to any limitation on the disclosure of the tax treatment or tax structure of any transaction or matter that is the subject of this communication and any attachments.