Article

Four lease accounting considerations for construction companies

June 26, 2022 · Authored by Jacqueline Stensland

The new lease accounting guidance impacts the construction industry in potentially unexpected ways.

Although the general provisions of the guidance and its application in many instances are straightforward, there are certain construction-specifics scenarios to consider, such as whether or not there are embedded leases within subcontractor or other arrangements and whether the amortization of leased assets used on a construction site should be included in project costs.

But first, let’s cover some basics.

Updates to lessee accounting for leases

The new lease accounting standard intends to provide users of financial statements with greater visibility and transparency into the financial impacts of a lessee’s lease obligations and leased assets.

Lessees are required to recognize all leases of property or equipment on their balance sheet. However, many will likely adopt an optional practical expedient whereby leases with terms of 12 months or less aren’t recognized as assets and liabilities on the lessee’s balance sheet but rather accounted for as executory contracts — similar to how operating leases were accounted for prior to the Financial Accounting Standards Board’s (FASB) new lease accounting guidance.

This may affect how an entity is evaluated by the users of its U.S. generally accepted accounting principles (GAAP) financial statements such as banks, investors, board members, and other stakeholders across a myriad of industries, including construction.

Effective dates

The FASB published accounting standards updated (ASU) 2016-02, Leases (Topic 842) in February 2016, which created accounting standards codification (ASC) Topic 842, Leases. Since issuing ASU 2016-02, the FASB deferred the effective dates of ASC Topic 842 for certain entities.

In June 2020, the FASB acknowledged that entities could face limited resources due to the COVID-19 pandemic and provided an additional one-year deferral of the effective date for certain entities. However, more recently the FASB made it clear that no further deferrals should be expected.

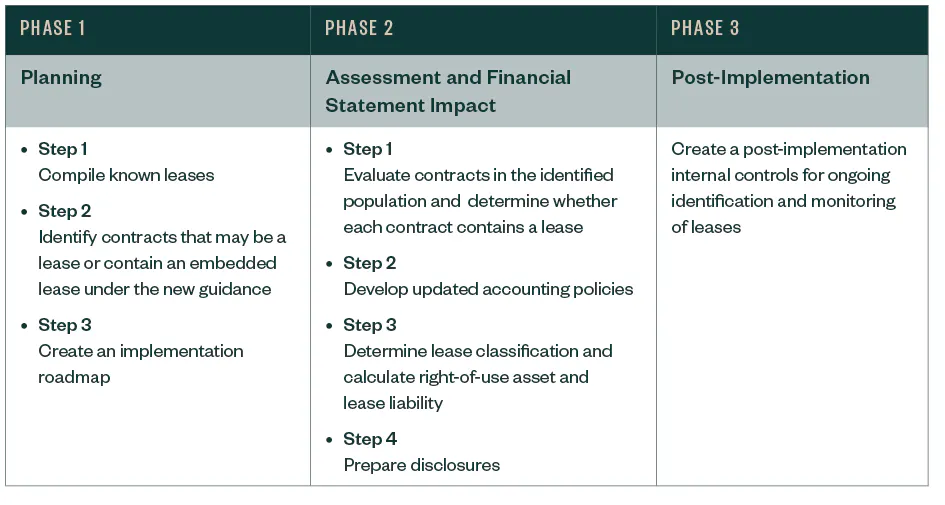

ASC 842 is effective for private companies for fiscal years beginning after Dec. 15, 2021 and interim periods within fiscal years beginning after Dec. 15, 2022. Although the reporting date for reflecting the adoption fast approaches, many construction companies have yet to start preparing to adopt this new accounting standard.