Article

Increase the potential of your tribal businesses with advanced business planning

Nov. 13, 2019 · Authored by Clayton Cafferata

For businesses of all sizes and scopes, effective planning can make the difference between failure and success. Without a plan, leaders are often left guessing about performance and whether or not they’re meeting key objectives.

This is especially true for tribal governments, which are tasked with creating sustainable communities and evaluating new business opportunities, while monitoring past and future directions of existing businesses.

Following is an overview of steps your tribal government can take to implement and benefit from a business plan.

Effective business plans

An effective plan can help your business achieve the following:

- Set expectations and incorporate accountability

- Track business metrics

- Communicate results to those responsible

- Incorporate directions for following up on results

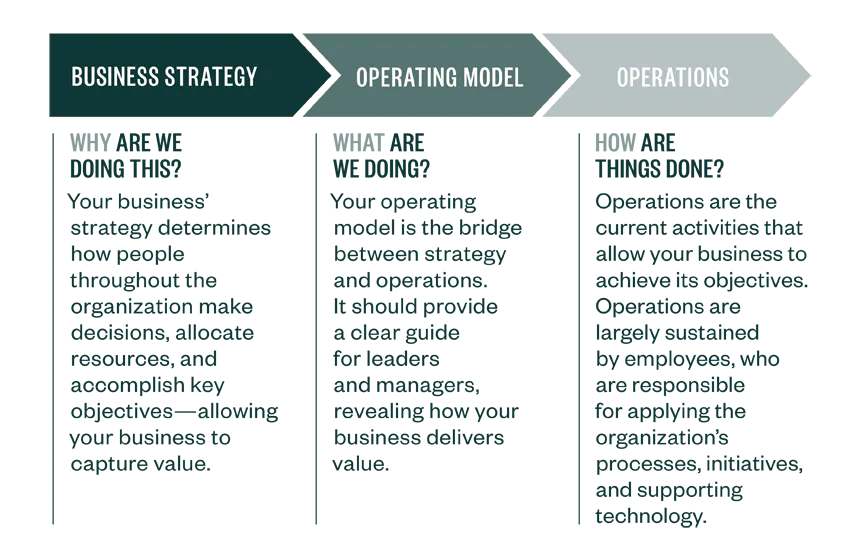

The graphic below identifies some key components of a business plan and how they’re related to one another.

Tribal business dynamics

Tribes can have a variety of businesses, including hotels, casinos, convenience stores, smoke shops, seafood companies, marijuana operations, golf courses, and many others.

Often, tribes have an enterprise board that oversees tribal businesses separately from the tribe’s governing body, or tribal council. The tribal council and the enterprise board must work together on the tribe’s business strategy development and deployment — executing a vision for economic and social development, evaluating new opportunities, and reviewing existing operations.

Unique factors

In the context of tribal businesses, there are additional unique factors that can impact your business plan’s success. These factors include:

- Supporting tribal member employment and wellbeing

- Capitalizing on unique competitive advantages of tribes, such as tax-exempt, federal contracting, and minority-owned business statuses

The information provided here is of a general nature and is not intended to address the specific circumstances of any individual or entity. In specific circumstances, the services of a professional should be sought. Tax information, if any, contained in this communication was not intended or written to be used by any person for the purpose of avoiding penalties, nor should such information be construed as an opinion upon which any person may rely. The intended recipients of this communication and any attachments are not subject to any limitation on the disclosure of the tax treatment or tax structure of any transaction or matter that is the subject of this communication and any attachments.