Article

Earnouts: Structures to mitigate price volatility in transactions

Oct. 31, 2023 · Authored by Akshaya Jaisankar

During a transaction, earnouts can bring significant reporting and valuation challenges that could impact the deal’s final results.

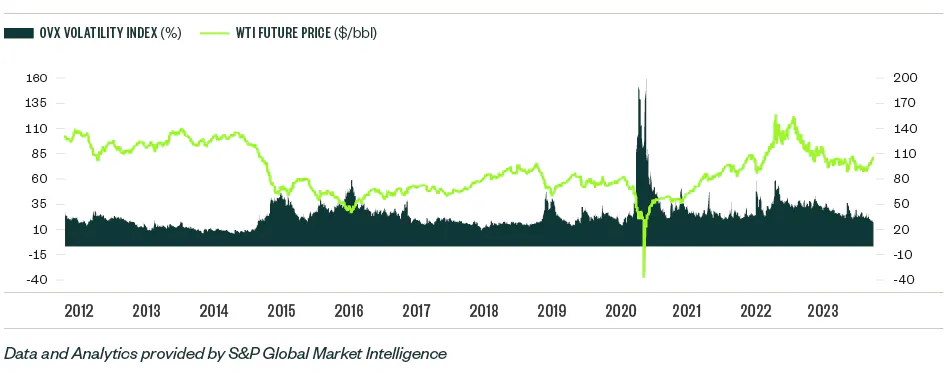

Oil and gas companies need to carefully review earnouts, especially during current market volatility as world events impact oil pricing.

Explore options to approach your accounting treatments, valuation approaches, and more to help reduce risk and prepare for potential future transactions.

What is an earnout?

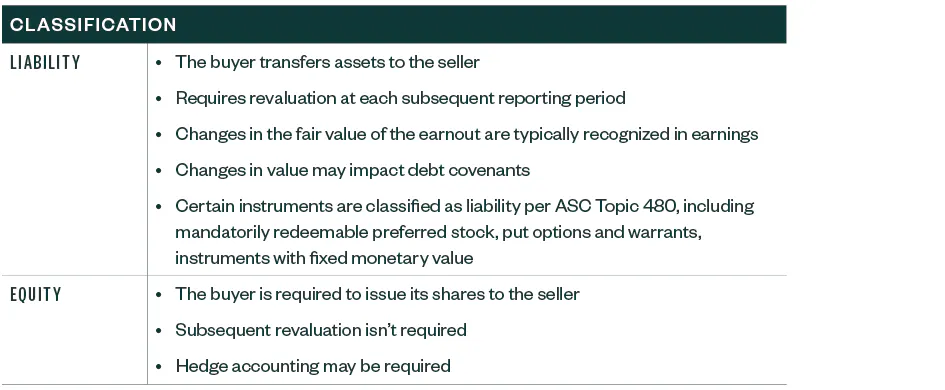

Earnouts are contingent, deferred payments used in transactions to reconcile differences in opinion between the buyer and the seller regarding the fair value of an asset.

Earnouts are contingent upon a metric or threshold being met in the future.

An earnout can help mitigate the buyer’s risk of overpaying and defer payment of a portion of the total consideration allowing for more financing options.

An earnout can give the seller the potential to increase the total consideration in exchange for delaying a portion of the payments.

In oil and gas, different types of earnouts are used depending on the stage of development of the asset:

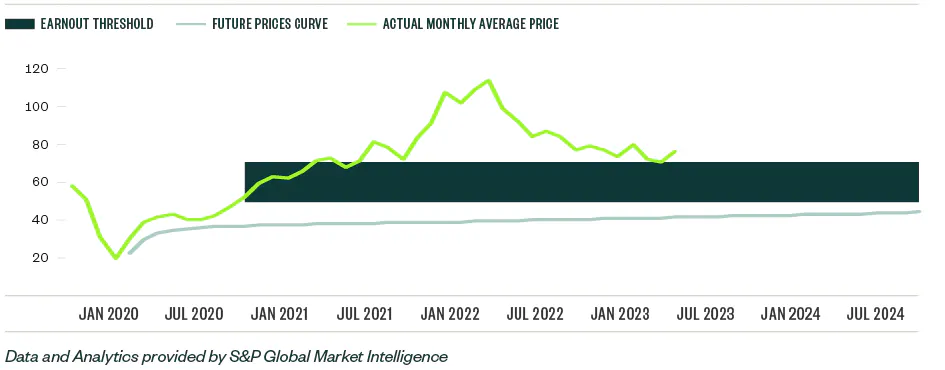

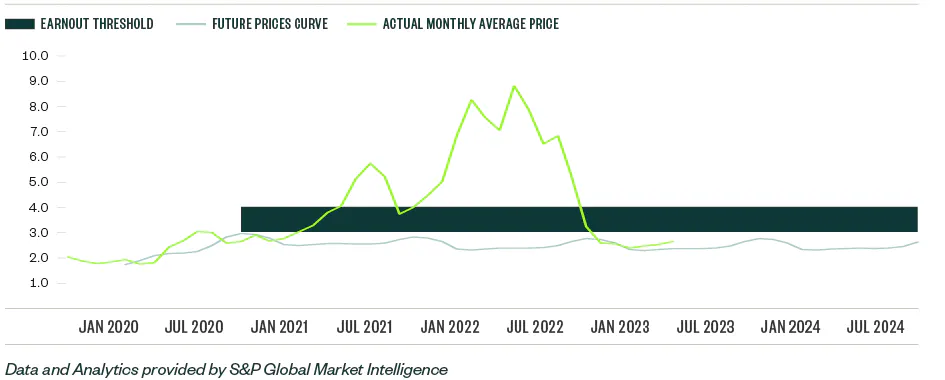

- Commodity price. Based on the price of a commodity index such as West Texas Intermediate (WTI) crude oil.

- Operational. Based on achieving milestones such as production volumes, earnings before interest, taxes, depreciation, and amortization (EBITDA) targets, and similar.

- Geological. Based on meeting exploration targets. Typically used in offshore assets.

Buyers and sellers should specify any calculations or features of the selected metric.

For example, if a commodity price is used, the agreement should specify the contract — prompt month, 12-month strip — as well as the publication source, such as NYMEX or Platts, and the time of the publication, such as daily closing price or average of the month.

Related sections

Declining oil and gas prices and impacts on your company’s financial reporting

The information provided here is of a general nature and is not intended to address the specific circumstances of any individual or entity. In specific circumstances, the services of a professional should be sought. Tax information, if any, contained in this communication was not intended or written to be used by any person for the purpose of avoiding penalties, nor should such information be construed as an opinion upon which any person may rely. The intended recipients of this communication and any attachments are not subject to any limitation on the disclosure of the tax treatment or tax structure of any transaction or matter that is the subject of this communication and any attachments.