Pass-through entity taxes permit the pass-through entity to pay the state tax at the entity level, and as the $10,000 SALT cap applies to individuals, the pass-through entity taxes are taken as a partnership or S corporation deduction, which flows through to the partners without limitation. The partners, members or shareholders of the pass-through entity that has paid the state pass-through entity tax either receive a credit against their state individual income tax liability or deduct their distributive share of income from their adjusted gross income in determining their state income tax liability.

Article

Pass-through entity tax 101

Since the Tax Cuts and Jobs Act of 2017 (TCJA) limited an individual’s state and local tax (SALT) deduction to $10,000, states have been exploring pass-through entity tax workarounds in response. Fast forward to November 2020 when the IRS gave guidance to allow state tax deductions at the pass-through entity level and opened the floodgates to states enacting pass-through entity taxes in the ensuing months, with New York being one of the latest.

As straightforward as it sounds, it really is far from it. Because every state has different regulations, not every pass-through entity will benefit the same.

Click the sections below to see pertinent state-by-state updates from Baker Tilly.

Virginia denies residents out-of-state credit for certain PTE taxes

Published on Jan. 5, 2022

On Dec. 28, 2021, the Virginia Department of Taxation ruled that a resident taxpayer may not claim an out-of-state credit allowed under Virginia Code §58.1-332, A tax imposed at the entity level is not attributable to the individual members and therefore not eligible for the out-of-state credit, unless the taxpayer is a shareholder of an S-corporation. A complete copy of the ruling can be found here.

The ruling was in response to the ever-evolving regime of pass-through entity (PTE) tax workarounds that have been deployed by several states following the 2017 Tax Cuts and Jobs Act, which limited an individual’s federal itemized state and local tax deduction to $10,000, and IRS Notice 2020-75, which allows for the federal deduction of payments by PTEs for state and local income taxes. PTE tax workarounds authorize the PTE to pay the state tax at the entity level, which flows through to the owners without limitation. The owners of the PTE can either receive a credit against their state individual income tax liability or deduct their distributive share of income from their adjusted gross income in determining their state income tax liability.

Takeaway

Even though owners would expect a federal tax benefit by the PTE tax workaround, Virginia’s ruling is a recent example of when an owner of certain PTEs could lose tax credits and face a higher effective tax rate.

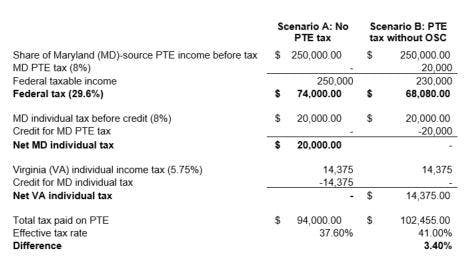

Consider the following example: A Virginia resident is an owner of an ineligible PTE that has Maryland sourced income.

Under Scenario A, the PTE does not elect to pay Maryland income tax at the entity level, and therefore, the Virginia owner enjoys the benefit of an out-of-state credit for their share of Maryland tax.

Under scenario B, assume that the PTE elects to pay Maryland income tax at the entity-level and the Virginia owner does not enjoy the benefit of an out-of-state credit. Under scenario B, the benefit of the federal deduction does not outweigh the cost of paying state taxes in Maryland and Virginia, and the Virginia owner would be taxed at a 3.4% higher effective rate.

The benefits of PTE tax workarounds are complex and require thorough modeling. PTEs and owners considering electing a new PTE tax regime are encouraged to connect with their Baker Tilly tax advisor.

New York State issues guidance as to filing PTET extensions and returns online

Published on March 11, 2022

In one of New York State’s PTET FAQs, the State has addressed what actions tax professional may undertake on behalf of their clients with respect to PTET electronically filings.

The following is an excerpt from the aforementioned FAQs that sets forth how tax professionals may establish that they are duly authorized tax professions with respect to a client’s PTET forms. As noted below, the FAQs reiterate that the annual election may not be made by a representative as they are not an authorized person.

“What actions can tax professionals with a Power of Attorney (POA) or an EZ Rep Tax Professional account take on behalf of their clients?

Duly authorized tax professionals may electronically file most PTET-related forms and returns on behalf of a client, including filing estimated payments, extensions, and the annual PTET return. However, the annual election may not be made by a representative as they are not an authorized person.

EZ Rep Tax Professional Account

The State will permit a tax professional to qualify as a Duly Authorized Tax Professional by establishing that the tax professional has an EZ Rep Tax Professional account for the client by timely filing Form TR 2000 with the State for each client in question.

New York State POA

Alternatively, the State will permit a tax professional to qualify as a duly authorized tax professional that may electronically file PTET related forms on behalf of the client if the tax professional has a timely filed New York State POA, Form POA-1, on file with the State.”

Caution: Authorized tax professionals performing PTET filings pose significant risks

The State’s PTET website states the following with respect to PTET tax online filings:

“The filing application allows the PTET entity to manually enter information for up to 100 eligible credit claimants. If the entity has more than 100 eligible credit claimants, it must upload a data file containing the information. The data file must be in a comma delimited format with a .txt or .csv extension. The PTET entity must include the following information for each eligible credit claimant:

- the claimant’s name and identification number;

- whether the claimant is claiming the credit through a direct partner who is a disregarded entity and if so, the name and identification number of the disregarded entity;

- the type of taxpayer claiming the PTET credit, such as an individual, estate, or trust;

- the claimant’s ownership percentage in the PTET entity;

- the claimant’s share of the PTET credit; and

- the residency status of the partner or member of a partnership as classified for PTET purposes (note: for PTET purposes all S corporation shareholders are treated as if they are nonresidents).”

The State’s PTET website further states the following:

“The filing application will allow a filer to save their work without filing and come back later to complete the return. It is important for the PTET entity to report this information correctly. The entity may not amend any of the reported information once the return has been submitted. If the entity omits any information for an owner or submits incorrect information, some or all credit claimants may not be allowed to claim their PTET credits.”

We wish to emphasize the State’s guidance as to the inability to amend or correct the information with respect to the PTE’s eligible credit claimants and the potential significant ramifications arising from incorrectly inputting such information, i.e. If the entity omits any information for an owner or submits incorrect information, some or all credit claimants may not be allowed to claim their PTET credits.

The potential ramifications arising from errors in the eligible credit claimant information should be carefully considered with respect to the decision to have Baker Tilly file the PTET extension or PTET return pursuant to the State’s expanded actions permitted by an authorized tax profession.

Citation: New York State frequently asked questions about pass-through entity tax (PTET)

New York updates PTET website with list of jurisdictions that are “substantially similar” as of Dec. 3

Published on Jan. 10, 2021

When New York adopted its pass-through entity tax (PTET) provisions, the State amended Section 620 – Credit for Income Tax of Another State.

In particular, New York amended Section 620 to include a new Section 620(b):

620(b)

Pass-through entity taxes

620(b)(1)

A resident shall be allowed a credit against the tax otherwise due pursuant to this article for any pass-through entity tax substantially similar to the tax imposed pursuant to article twenty-four-A of this chapter imposed on the income of a partnership or S corporation of which the resident is a partner, member or shareholder for the taxable year by another state of the United States, a political subdivision of such state, or the District of Columbia upon income both derived therefrom and subject to tax under this article.

In August 2021, New York issued TSB-M-21-(1)C, (1)I that stated, in part, that “A list of substantially similar taxes that qualify for the resident tax credit will be posted on our website”. The State updated their PTET website to include a list of jurisdictions that have adopted, as of Dec. 3, 2021, PTE taxes that the State deems to be qualifying as “substantially similar.”

The State has recognized 20 states – view the list here.

Important points to note:

- The list does not include North Carolina – This may be an oversight as North Carolina’s PTE tax provisions were adopted on Nov. 30, 2021.

- The list does not include Michigan – Michigan adopted PTET provisions subsequent to Dec. 3, 2021.

- The list includes the Ohio Non Resident Withholding Tax per Ohio Section 5747.41.

We expect New York to add to North Carolina and Michigan upon updating the list.

New York's pass-through entity tax deadline is Oct. 15

New York's version of the tax

Published on Sept. 18, 2021

New York’s PTET is for eligible partnerships, including limited liability companies, and S corporations to make an annual, optional and irrevocable election to pay tax on certain income for tax years beginning on or after Jan. 1, 2021. For the 2021 tax year, an entity must make the election through the state’s business online services account portal by Oct. 15, 2021.

The final day for deciding whether to make the irrevocable election for the 2022 tax year is March 15, 2022.

Before a pass-through entity decides to make the election, it should take into consideration how the calculation of PTET taxable income differs between electing New York S corporations and electing partnerships. The pass-through entity should work with its tax advisor to determine what its taxable income would be as well as its corresponding liability for federal and state tax and credit for taxes paid.

Even though a pass-through entity would expect a federal tax benefit by making the election, it is possible an individual will lose some of their tax credits for taxes paid to other jurisdictions. The risk of losing the credit should be considered prior to making a pass-through entity tax election.

If the pass-through entity decides to move forward, an authorized person, as defined by New York statutes, makes the election, which is binding on all partners, members or shareholders of the pass-through entity.

For tax year 2021, electing entities are not required to make estimated tax payments. However, partners, members and shareholders of electing pass-through entities must continue to make estimated tax payments as if they were not entitled to the PTET credit.

Eligible taxpayers must file an individual personal income tax return to claim the PTET credit. The PTET credit may not be claimed on a group return (composite return) for nonresident partners and shareholders. Individual, trust or estate partners and shareholders will be able to take a credit equal to 100% of the New York PTET paid on their behalf by the pass-through entity. A taxpayer may not claim a PTET credit unless the electing partnership or S corporation paid the tax and the pass-through entity supplies sufficient information on its tax return to identify the taxpayer who will claim the credit. Any overpayment in New York PTET will be credited or refunded to the individual without interest.

In whatever way the pass-through entity is affected by the PTET, the mechanics of claiming the credit for taxes paid is fraught with risk and uncertainty. For example, it still hasn’t been resolved whether individual and/or composite returns are required or allowed or what happens to an entity’s net operating losses. Careful analysis of the taxpayer’s overall tax attributes and state law nuances is required to understand the full impact to both federal and state taxes.

The information provided here is of a general nature and is not intended to address the specific circumstances of any individual or entity. In specific circumstances, the services of a professional should be sought. Tax information, if any, contained in this communication was not intended or written to be used by any person for the purpose of avoiding penalties, nor should such information be construed as an opinion upon which any person may rely. The intended recipients of this communication and any attachments are not subject to any limitation on the disclosure of the tax treatment or tax structure of any transaction or matter that is the subject of this communication and any attachments.