Dynamic Costing®: empower operations to impact EBITDA

One approach manufacturers can take on their journey toward Industry 4.0’s goal of continuous improvement comes from enabling transparency of the true product cost drivers, specifically by the implementation of Dynamic Costing™.

Traditional standard costs can be helpful when looking at certain static business lines a manufacturer produces, but as production mixes at the plant are now changing faster than ever before, using only those historical standards may be hurting the organization’s actual overall equipment effectiveness (OEE) by focusing on the “low cost product” blind to its impact on through put. Most importantly, it may even be damaging the manufacturer’s bottom line by not having a proper understanding of which products are responsible for driving profitability today.

In the recent webinar sponsored by the Original Equipment Suppliers Association (OESA), “Industry 4.0: Gauging your enterprise technology and the power of integration,” members of Baker Tilly’s supply chain and manufacturing consulting practice Peter Pearce, principal and practice leader, and Cameron Reid, director, discussed how Baker Tilly’s Dynamic Costing could help a manufacturer more reliably determine the range of its actual costs.

Depending on a manufacturer’s industry 4.0 maturity level, an organization may be able to leverage its existing information to enable Dynamic Costing. In turn, those insights can drive business results and help the organization make informed decisions in a rapid time frame.

Traditional standard costing versus Dynamic Costing

The main components of traditional standard costing are materials, labor, fixed overhead and variable overhead — but are not the only components that should be factored into a business’s costs.

The data gathered when using the standard cost accounting method is most likely aggregate averages that lags current production. Standard costing depends on snapshots of costs for a given total period in time for most of its data, which creates challenges to see within a narrower production time window. Information used in this type of costing is not updated frequently and as a result it does not provide for a clear understanding of root cause for when a cost variance occurs. Without real-time data driving the costing models, manufacturers will lose the opportunity to see the detrimental effects on plant throughput, worker efficiency and product quality.

These should be reason enough to leave traditional standard costing behind, but Pearce said, “the real reason standard costing is becoming obsolete is customers are only going to pay a certain amount for a product regardless of what it costs an organization to make it. The market drives the price and a company needs to be prepared to pivot to what they can manufacture to keep up with the price the customer demands.”

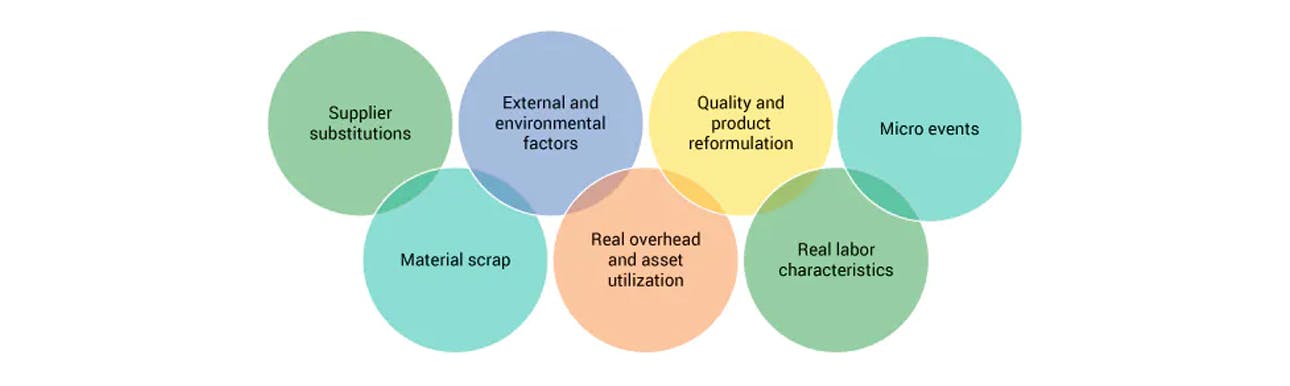

Dynamic Costing measures real labor, real material consumption, real overhead and asset utilization, environmental factors, quality; scrap, and micro events that are tied to assets (e.g., shift changeovers, equipment downtime, etc.).

Benefits of Dynamic Costing

Moving from cost accounting to cost management analytics is a significant advantage when using Dynamic Costing. Another benefit is being able to use real-time information, allowing an organization to be responsive to market changes. Dynamic Costing incorporates the intangibles that standard costing ignores, e.g., micro-events like equipment failure as well as quality, scheduling, scrap, environmental factors and suppliers and their materials. Separately, these costs may not seem to make an enormous difference to an organization’s bottom line, but together, they can add up quickly. Finally, it focuses on reducing costs across the enterprise versus looking at a specific product.

To move toward Dynamic Costing, an organization will need some Industry 4.0 enabling tools. Data analytics is an “enabler” that will provide manufacturers with statistically meaningful information to help them make real-time decisions quickly — but only if they are tapping into the right information. This is where integration comes in. “An organization’s production technology should be integrated using a solution set, such as Plex, IFS, Oracle and other transactional business systems, which supports the needs and demands of Industry 4.0, from the top floor to the shop floor,” Pearce said. For instance, it should connect manufacturing assets with the financial department of the business, so they can really tune into what is happening immediately within the operation.

Dynamic Costing

Baker Tilly has contextualized a five-step Dynamic Costing road map to execution within the Industry 4.0 environment below.

Step 1: Planning

One of the first things an organization needs to do is to identify its business objectives. For most organizations, their business objectives change over time. Reid said, “For example, when a manufacturer starts an initiative, it is solely looking to maximize profit. When a “black swan” event occurs, e.g., a pandemic, the manufacturer has to shift from maximizing profit to surviving.” Having an Industry 4.0 structure in place provides flexibility and allows it to rapidly change its business objectives and make appropriate decisions.

Another part of planning is assessing systems or infrastructure, whether it be software or staff, and making sure the organization has suitable tools and resources available. Lastly, by looking at its culture and structure, an organization can determine how it is progressing along the maturity continuum.

Step 2: Gather data and analyzing operations

An organization must understand the true source of data it’s using to make decisions. It could be from internal sources, such as its enterprise resource planning (ERP) system, manufacturing execution system (MES), or even spreadsheets. It may also come from external sources, like a third-party payroll administrator.

A manufacturer should also be looking at its hardware needs — programmable logic controllers (PLCs) on the shop floor, human machine interfaces (HMIs), scales, robots, etc. — and if it has devices and machinery that can be included in the IIoT environment. When it has the right hardware, it will be able to identify where that data is and how to collect it.

Gathering data is also where an organization should be taking stock of its master data. Reviewing that master data and ensuring its accuracy is critical to that process because otherwise “garbage in, garbage out” is not just a saying, but an actuality for that organization.

Step 3: Build a program to assimilate information

This step is not based entirely on merely building an application for accessing information; it is also about putting in place the controls necessary to ensure movement along the continuum of Industry 4.0 is sustainable. The organization needs to have the correct technology to leverage this information, as well as the management wherewithal to capitalize on the information that is available.

Other items critical to this step are:

- The utilization of extract, transform, load (ETL) tools in terms of defining analytic workflows (both process and data workflows) and to the sustainability of the overall process

- The development of integration maps, which indicate where the organization is getting information and where there are possible gaps in the data

- The deployment of an analytic framework and associated models, showing how data and analytics flow

Step 4: Implement and validate against business objectives

When first talking about an implementation, the organization often focuses on business objectives, but when it is time to get into the details of an implementation plan, those objectives are put on the back burner. It is important to continually validate against the business objectives and ensure the solution put in place supports the organization.

At this step, an organization should assign a dedicated project champion to stay focused on the objectives, and demonstrate the benefits of the solution to team members as well as the employee base. The organization should review results against business objectives and then validate product level results to achieve confidence with a top-down view.

The final part in this step is communication. At every stage within an Industry 4.0 deployment, Reid said, someone should be asking, “Is this appropriate for the organization?” It should be an open communication so everyone is confident the technologies being put forth are going to be beneficial to the organization.

Step 5: Institutionalize Dynamic Costing

Organizations now have the tools to collect and analyze data to make decisions rapidly and continuously over time. With Industry 4.0 integration of shop machinery to back-end systems, manufacturers have real-time information at their fingertips. Processes and procedures should be defined and implemented in order to make the institutionalization and continuous improvement aspect of this a reality. If an organization does not revisit improvements, it will either not progress or, worst-case scenario, slide back into previous behaviors.

Finally, with Industry 4.0, manufacturers deal with contingency planning and should perform “what-if” scenarios, working with the technology that is in place. It gives the organization the capacity to analyze and take action upon near real-time information. If organizations look back to what issues they were talking about in December 2019 or January 2020, the conversations they are having now are much different. It is that ability to rapidly pivot on what their objectives are that will be key to their success over time.

For more on this topic, please visit Baker Tilly’s Dynamic Costing services page.