Bonus depreciation rules, recovery periods for real property and section 179 expensing

The Tax Cuts and Jobs Act (TCJA or the Act) made many changes to the depreciation and expensing rules for business assets. This tax alert will focus on three major provisions of the final legislation:

- Sunsetting bonus depreciation

- Applicable recovery periods for real property

- Expansion of section 179 expensing

Below we revisit provisions by individual topic, followed by a discussion of various considerations and tax planning opportunities.

Bonus depreciation

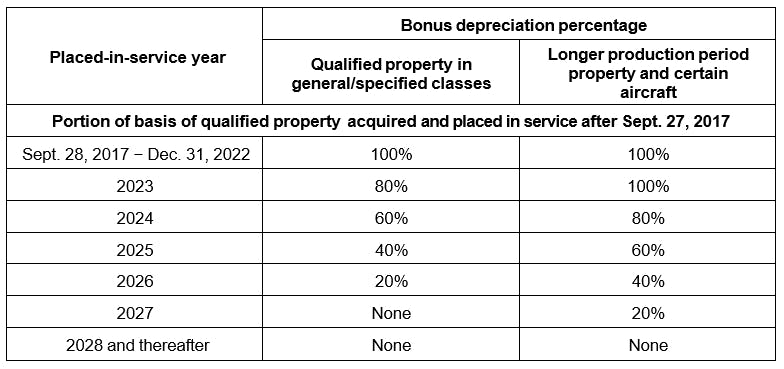

Businesses may take 100% bonus depreciation on qualified property both acquired and placed in service after Sept. 27, 2017, and before Jan. 1, 2023. The acquisition date for property acquired pursuant to a written binding contract is the date of such contract and may have extended bonus periods. Full bonus depreciation is phased down by 20% each year for property placed in service after Dec. 31, 2022, and before Jan. 1, 2027.

Under the new law, the bonus depreciation rates are as follows:

A transition rule provides that for a taxpayer’s first taxable year ending after Sept. 27, 2017, the taxpayer may elect to apply a 50% allowance instead of the 100% allowance. Taxpayers can still elect not to claim bonus depreciation for any class of property placed in service during any tax year. The election out of bonus depreciation is an annual election.

Due to the repeal of the corporate alternative minimum tax, the legislation also repealed the election to claim minimum tax credits in lieu of bonus depreciation for tax years beginning after 2017.

Qualified property

Under the law, qualified property is defined as tangible property with a recovery period of 20 years or less. The law eliminated the requirement that the original use of the qualified property begin with the taxpayer, as long as the taxpayer had not previously used the acquired property and the property was not acquired from a related party. The inclusion of used property has been a significant, and favorable, change from previous bonus depreciation rules.

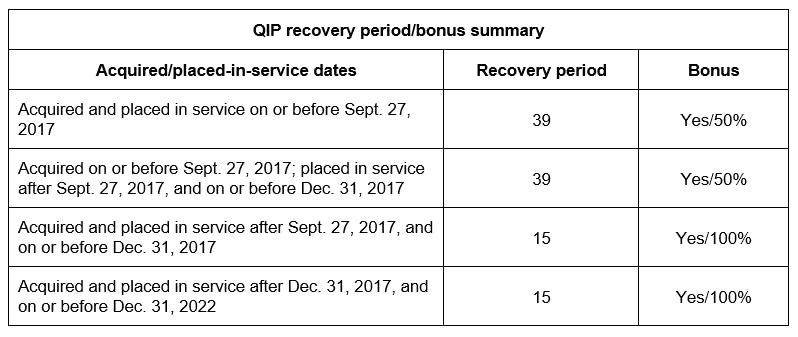

Subsequent modifications to the original law clarified bonus depreciation rules for qualified improvement property (QIP). The CARES Act permanently codified that QIP has a 15-year recovery period as well as the 20-year alternative depreciation system (ADS) recovery period. As a 15-year asset, QIP is eligible for 100% bonus depreciation through 2022 and the sunsetting bonus depreciation percentages through 2026.

Lastly, qualified property does not include: 1) property used in providing certain utility services if the rates for furnishing those services are subject to ratemaking by a governmental entity or instrumentality, or by a public utility commission; 2) any property used in a trade or business that has floor plan financing indebtedness; and 3) property used in a real property trade or business that makes an irrevocable election out of the interest expense deduction limitation under section 163(j). Under the interest expensing provisions, these entities would have to depreciate residential real property, nonresidential real property and QIP under the ADS lives and methods. Therefore, such property would not be eligible for bonus depreciation.

Applicable recovery periods for real property

The Act retained the current Modified Accelerated Cost Recovery System (MACRS) recovery periods of 39 and 27.5 years for nonresidential and residential rental property, respectively. However, the ADS recovery period for residential rental property was reduced to 30 years from 40 years effective for property placed in service on or after Jan. 1, 2018.

The Act eliminated the separate definitions of qualified leasehold improvement, qualified restaurant, and qualified retail improvement property. Instead, the Act provides simplification with a general 15-year recovery period for QIP (and 20-year ADS recovery period). QIP is any improvement to an interior portion of a building that is nonresidential real property if the improvement is placed in service after the date the building was first placed in service, excluding: enlargements, elevators/escalators and internal structural framework. The improvements do not need to be made pursuant to a lease.

Electing real property trades or businesses

As noted above, a real property trade or business that elects out of the interest expense deduction limitation must use ADS to depreciate nonresidential real property (40 years), residential rental property (30 years) and QIP (20 years). The modifications to the ADS recovery period for residential rental property (40 years to 30 years) as well as the 20-year ADS recovery period for QIP (versus 40-year under pre-Act law) may provide an opportunity for certain taxpayers in real property trades or businesses to shorten their recovery periods while at the same time electing out of the interest limitation. An election out would require taxpayers to treat a change in the recovery period and method as a change in use (if affecting property already placed in service for the year the election is made).

Subsequent changes to the law (section 202 of Taxpayer Certainty and Disaster Tax Relief Act of 2020) now allow for taxpayers with residential real property placed in service before Jan. 1, 2018, to file a “change in use” automatic change in accounting method to correct 40-year ADS life to 30-year ADS life. This automatic accounting method change will generally result in a catch-up depreciation deduction.

Expansion of section 179 expensing

The Act increased the maximum amount a taxpayer may expense under section 179 to $1 million with annual increases indexed for inflation. The current 2022 section 179 limit is $1.08 million. The investment limit (also referred to as the total amount of equipment purchased or phase-out threshold) was also increased to $2.5 million with the indexed 2022 limit is $2.7 million. The current $1.08 million limitation is reduced (but not below zero) by the amount by which the cost of qualifying property placed in service during the taxable year exceeds $2.7 million. Expect and review for annual inflation adjustments.

The TCJA also expanded the definition of section 179 property to include certain depreciable tangible personal property used predominately to furnish lodging or in connection with furnishing lodging (i.e., beds or furniture used in hotels and apartment buildings). The definition of qualified real property for section 179 purposes was also expanded to include any of the following improvements made to nonresidential real property: roofs, exterior heating, ventilation and air-conditioning property, fire protection and alarm systems and security systems as long as the improvements are placed in service after the date the building was first placed in service.

Planning considerations

These expensing and cost recovery rules may significantly change the analysis for cost recovery, similar to when the de minimis election and other elections and accounting methods were added under the repair regulations. Determining the appropriate tax treatment for tangible property expenditures may require a “decision tree” analysis beginning with identification of items that qualify for a current deduction under existing rules (i.e., repairs or incidental materials and supplies), then identifying other exceptions and applying as appropriate. For example, a taxpayer may first apply conformity to financial statement expensing, where possible, using the de minimis rules. Then, apply bonus depreciation and section 179 for items ineligible under the de minimis rules, considering respective eligibility and phase-out thresholds to maximize the tax benefit.

Bonus versus section 179. Consideration and comparison of bonus depreciation and section 179 is critical in planning for depreciation deductions. Both result in substantial present value tax savings for businesses that already had plans to purchase or construct qualified property. Unlike section 179 expensing, however, taxpayers do not need net income to take bonus depreciation deductions. Additional tax planning in relation to the new net operating loss (NOL) limitations – as well as the new limitation on losses of noncorporate taxpayers – will be necessary in these situations. Further, bonus depreciation is not limited to smaller businesses or capped at a certain dollar level as under section 179, where larger businesses that spend more than the investment limitation on equipment will not receive the deduction. Lastly, the years in which full expensing is available may offset the impact where the section 179 deduction may not be allowed due to either the expensing or investment limitations.

Qualified real property under section 179. The increase in both the section 179 expense and investment limitations as well as the expansion of the definition of qualified real property would also provide immediate expensing to taxpayers that invest in certain qualified real property (especially for property that is not eligible for bonus depreciation). The expanded definition of real property under section 179 may also be able to offset situations in which certain building replacement property would have otherwise been capitalized under the repair regulations (if on a repairs method). For example, if under the repairs analysis, it is determined that one of two HVAC units requires capitalization under the restoration rules, the unit may be qualified real property and deducted as a section 179 expense, assuming within the expensing and investment limitations.

State decoupling. Many states have decoupled from bonus depreciation, qualified improvement property as well as the increased percent 179 amounts.

Used property. Including used property in the definition of qualified property for bonus depreciation has a potentially significant impact on M&A restructuring as bonus depreciation now applies to qualified property acquired in a taxable acquisition. In asset acquisitions, either actual or deemed under section 338, capitalized costs added to the adjusted basis of the acquired property may be able to be fully expensed if allocable to qualified property. Structuring taxable transactions as asset purchases rather than stock acquisitions may result in an immediate deduction of a portion of the purchase price in the acquisition year or generate NOLs that have favorable tax planning consequences in connection with the new NOL rules.

Placed-in-service date. Because of the significant impact of 100% bonus depreciation, more scrutiny is anticipated around the determination of the placed-in-service date of an asset. With the sunsetting of bonus depreciation during 2023-2026, taxpayers will generally want an earlier placed-in-service date in order to maximize bonus depreciation deductions.

For depreciation purposes, property is considered placed in service when the asset is ready and available for use in its intended function. Taxpayers often acquire depreciable assets such as machinery and equipment before they begin their intended income-producing activity. In these situations, generally depreciation deductions may not be claimed for the machinery and equipment before the taxpayer’s business starts and the depreciating asset is used in that activity. Both acquisition and placed-in-service dates will require a detailed review of the facts and circumstances to make sure the appropriate bonus depreciation allowance is claimed.

Elections. Elections that reduce annual depreciation deductions (election out of bonus depreciation, annual election to use ADS, etc.) will also become more critical in tax years beginning on or after Jan. 1, 2022, when depreciation deductions will reduce "adjusted taxable income" for purposes of the interest deduction limitation. It will become increasingly important to model out the impact of various depreciation elections for planning purposes.

Cost segregation studies. Consideration of a cost segregation study is now more important than ever. A cost segregation study is an in-depth analysis of the costs associated with the construction, acquisition or renovation of owned or leased buildings for proper tax classification and identification of assets that may be eligible for shorter tax recovery periods resulting in accelerated depreciation deductions. The reclassification of assets from longer to shorter tax recovery periods also make these assets eligible for bonus depreciation resulting in even more substantial present value tax savings, especially with 100% bonus depreciation for qualified property placed in service from Sept. 28, 2017 through the end of 2022. Tangible personal property and land improvements identified in the cost segregations of acquired property placed in service after Sept. 27, 2017, are now qualified property for bonus depreciation purposes since the definition of qualified property was expanded to include used property.

Cost segregation is especially critical to real property trade or businesses that may not claim bonus depreciation on QIP because of the election out of the interest deduction limitation. These entities may desire the tax benefit from the reclassification of personal property to shorter tax recovery periods resulting in accelerated depreciation deductions. The modification to the recovery period under ADS (to 30 years from 40 for property placed in service after Dec. 31, 2017) for residential rental property, as well as the 20-year ADS recovery period for QIP, also provides these real estate taxpayers with the ability to recover real property over shorter recovery periods.

The IRS provides numerous automatic changes in accounting methods for missed opportunities to segregate bonus eligible assets and claim a catch-up section 481(a) deduction. These deductions can be significant with the filing on the Form 3115.

Taxpayers should balance the numerous options with their fixed asset additions, renovations, and remodels. The repairs and maintenance regulations may provide deduction opportunities that both simplify reporting and deductions for states not complying with bonus depreciation. In cases where 100% bonus for QIP additions are the facts, there may be a second opportunity to take a partial asset disposal deduction on the abandoned assets replaced by the QIP.

For related insights and in-depth analysis, see our tax reform resource center.

For more information on this topic, or to learn how Baker Tilly tax specialists can help, contact our team.

The information provided here is of a general nature and is not intended to address the specific circumstances of any individual or entity. In specific circumstances, the services of a professional should be sought. Tax information, if any, contained in this communication was not intended or written to be used by any person for the purpose of avoiding penalties, nor should such information be construed as an opinion upon which any person may rely. The intended recipients of this communication and any attachments are not subject to any limitation on the disclosure of the tax treatment or tax structure of any transaction or matter that is the subject of this communication and any attachments.